Digital finance has become one of the most important tools to accelerate the financial inclusion in the recent years.

--BY Nikeeta Gautam

In a world where many services have become digitized, digital finance has come upfront as a powerful medium of providing financial services, especially to people with little or no access to financial services. The term ‘digital finance’ means providing financial services to the masses using the platforms of mobile solutions, internet and digital payment.

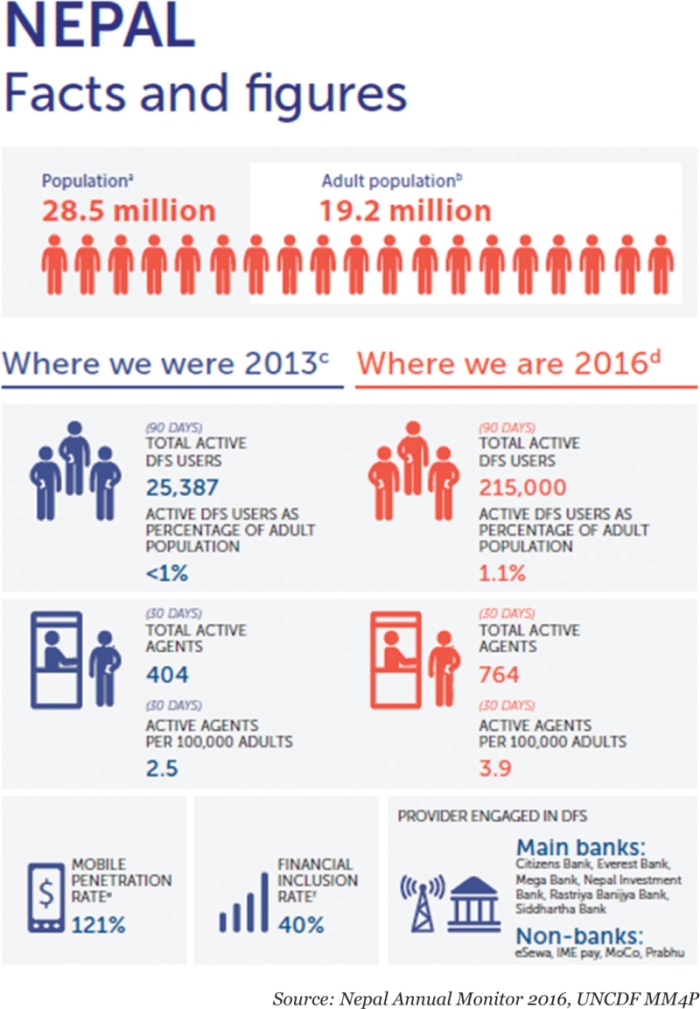

It is estimated that only about 40 percent of the population in Nepal presently has access to financial services through banks and financial institutions (BFIs). According to the United Nations Capital Development Fund (UNCDF) - MM4P programme in Nepal, only 40 percent of the adult population have savings account in banks. It is the low level of access to modern financial services and unavailability of banks and Financial institutions (BFIs) causing farmers and entrepreneurs in rural areas to remain financially excluded. Long travel distances, tiresome procedures to open bank accounts and high associated costs are some of the reasons many Nepali citizens have remained unbanked.

Current scenario of access to digital finance

Nepal is a cash dominated economy where only 19 percent of transactions take place in bank cheques and less than 10 percent of transactions are done in digital form.“72 percent of the transactions in Nepal take place in cash,” says Jaspreet Singh, Country Technical Specialist of Digital Finance for UNCDF’s MM4P programmein Nepal.

Despite this situation, the country has seen growing rate of penetration of mobile internet and number of users in the last four years. “The penetration of ATM has been growing at the steady rate of 7-8 percent annually and the debit card users are also growing by the same rate," he says. Singh mentions that banks have been adding new card holders. “But this does not mean that everyone is an active user of such banking service. Hardly, 50-60 percent of card holders are active users," Singh adds. "While talking about active users, we typically count how many people have used their ATM cards for cash withdrawal and payment purposes in the last 90-days."

The Monetary Policy for FY 2017/18 published by the Nepal Rastra Bank shows that the number of ATM outlets has reached 2,047 across the country with the number of debit cards issued by BFIs totaling 5.18 million as of April, 2017. Similarly, the number of subscribers of mobile and internet banking services have reached 2.42 million and 735,000 in the period.

A number of issues have been obstructing the growth of digital finance service (DFS) market in Nepal. "Apart from the low level of digital financial literacy, there is also the issue of the banking sector taking the proper approach to educate customers. When BFIs offer service to their customers, the impact also depends on how they communicate about the services. For instance, when the banks distribute debit cards, they usually do not inform customers about the process to use the cards," opines Singh. “In case of rural areas, the use of debit cards is almost non-existent. It is because the majority of rural residents do not have bank accounts,” he adds.

All these clearly indicate that digital finance is still in its infancy in Nepal. However, the scenario seems to be changing with the NRB starting to issue licenses to non-bank payment service providers. These licenses are providing confidence to non-banking institutions to engage in setting up agent networks, develop partnerships, and introduce new and innovative DFS products. "There are non-banking financial service providers including IME, eSewa and Prabhu who recently received license for DFS. The pace of DFS is likely to gain momentum as more service providers will enter the market driving the competition in this business," says Singh adding that theNepali banking sector has been undergoing a lot of changes in the recent years due to merger, acquisitions and consolidation and BFIs have concentrated their efforts in managing core areas of credit and deposit. Nevertheless, few banks such as Citizens Bank, Everest Bank, Mega Bank, Nepal Investment Bank, Machhapuchchhre Bank, Rastriya Banijya Bank and Siddhartha Bank are engaged in providing different types of DFS.

According to Nepal Annual Monitor 2016 published by UNCDF-MM4P in Nepal, NRB is also working on various policy initiatives, such as the National Retail Payment Strategy, and investing in an e-mapping system to track market progress.

The role of banking and non-banking institutions

With the ongoing consolidation in the banking sector, Nepali banks are trying to strengthen their positions in corporate, retail and SME segments. “They want to go to rural areas. But when it comes to creating an outreach channel, banks have taken a backseat,” says Singh. He views that this is not because of their unwillingness, but due to the lack of proper infrastructure to start banking services in rural and remote areas of the country. This is where mobile money comes in to increase rural people’s opportunities to access financial services. The role of mobile telecommunication service providers is important in this regard. "While bank's role can be major in managing the flow of money, mobile network operators can come ahead to create distribution channels," he says. In a country, where the mobile penetration rate is around 121 percent, third-party providers can have a very big role in financial inclusion. UNCDF-MM4P has also supported a few non-bank services in its initial stage of product development. Among other things, the technical assistance helped these mobile services providers to build the technology required for such services. "Now, these channels (non-banking services) have started to come up-front to build an agent network. Commercial banks have joined them as partners because these platforms are good at distribution of financial services," he shares.

The UNCDF MM4P Initiative

MM4P is a global initiative of UNCDF which was started in 2013 in a few countries including Benin, Liberia, Zambia, Malawi, Uganda, Lao PDR, Senegal and Nepal. In Nepal, the initiative has been funded jointly by Australian Aid, Metlife Foundation, Swedish International Development Cooperation Agency (SIDA), UNNATI A2F programme, United States Agency for International Development (USAID) and UNCDF. Set up to support the inception and development of digital financial services, the programme mixes financial, technical and policy support to help build robust DFS ecosystems in the least developed countries. According to Singh, every market has four stages of development. The first is the inception stage followed by startup, expansion and consolidation stages. "When we started working in Nepal, the market of digital finance was in the inception stage. Lot of players were working in 'silos' in which different group of companies were trying to create their own network. Rules and regulations for the new financial service were not in place," he says. The market has developed to the early stage and late stage of startup phase, albeit in a slow pace.

The UNCDF-MM4P works in six pillars of the DFS ecosystem that include policy and regulations, infrastructure, providers, distribution, high volume and customers. "UNCDF targets to make 10 percent adult population active in mobile money," he says. MM4P refers ‘active population’ to the customers who have not just opened bank accounts but also those who have used agents and other digital channels in the last five years for financial transactions. As per the Nepal Annual Monitor 2016, the percent of adult Nepalis active in using DFS was 1 percent in 2013 which has now reached to 1.1 percent.

The high volume payments refer to payments that can be made digitally and that are transfers by one institution to many recipients payments such as social security allowances. The Department of Civil Registration (DoCR) under the Ministry of Federal Affairs and Local Development (MoFALD) has planned to manage the payments through electronic medium of social security allowances for senior citizens and unemployed youths. For this, The World Bank and UNCDF-MM4P have join hands to provide technical assistance to DoCR to implement the e-payment strategy. Singh thinks that distributing payments in this way will gradually familiarise rural people in using digital services for financial transactions. "When people start using digital money, their doubts about the reliability of these services will slowly go away. Thus it will increase their awareness about digital finance," he opines.

The UNCDF-MM4P has been organising various activities such as coordinating workshops related to DFS, working with NRB on data analytics and capacity building through DFS-focused training and exposure visits to countries and institutions that have advanced in DFS. These activities have helped BFIs and non-banking financial institutions to launch new digital products. Furthermore, UNCDF MM4P has assisted the government to transit payments digitally through formal financial channels and has worked with the private sector institutions to develop a culture of customer-oriented innovations.

With an aim to take the DFS market into expansion phase, UNCDF has planned to continue investing in the MM4P programme for the next three years. The organization has moved ahead with a few projects in this regard such as supporting agri-tech companies in prototyping and testing of digital payment systems, assisting in the creation and piloting of youth focused products and helping women and migrants to access payment services.

Realizing the importance of digitalisation for financial inclusion, the government of late has showed interest in playing the role of a catalyst in such initiatives. "The last two policy statements of Budget and Monetary Policy are the testimonies that the government has been trying to broaden financial inclusion through digitised payments of social security allowances and the One household, One account initiative,” Singh expresses. Similarly, the country’s private sector has also come to the forefront to the changes in the financial system as many institutions have been adopting digital technologies in order to provide services efficiently.

While financial inclusion has become discourse of utmost importance for policymakers, bankers and general public in the recent years, it is important to think about the technology to deliver financial services.

Experts suggest that policymakers and regulators should get used to technologies for DFS before formulating and implementing policies. “The central bank and the policymakers need to take some time to align themselves to the changing technologies in order to set appropriate rules and regulations,” he shares. According to him, as the required infrastructure and policy for digital finance have not been set yet, the government also needs to work on procedural changes before taking the decision. “And if the government takes decision in a short time, there are chances that things might not go as planned," he cautions.

Speeding up digital finance

In the present day world, digital financial services play a crucial role in financial inclusion and this has been the top priority of policymakers in many countries. The World Bank under its Universal Financial Access 2020 (UFA2020) has targeted to enable adults of the world, who aren’t part of the formal financial system, to have access to the financial system by 2020. Digital finance also plays a vital role in reducing poverty as the people even in rural areas can get the financial services at low costs. Besides this, this will also help in controlling the informal sources of lending money that are considered very exploitative particularly in rural areas.

NRB has adopted data driven decision making process for the implementation of policy and programmes, with interoperability as a major theme, according to Nepal Annual Monitor Report 2016 published by UNCDF-MM4P,. Technically, interoperability is the ability of computer systems to engage in exchange and use of available information. In a country with diverse geography, it is difficult for BFIs to open branches in all areas. This is where interoperability comes in as the major factor for speeding up the process of digital financing. “Investing in interoperability is worthwhile and sustainable for the private sector. It will help in speedy expansion of the DFS market in Nepal,” opines Singh.

There are, however, many other factors to ensure the success of DFS services in the country. Dialogue between the public and private sectors, for example, can turn the initiatives in digital finance successful in the long run, experts say. “Like other sectors, DFS also needs a dialogue mechanism between public and private sector. At present, the implementation of policies usually followstop-down approach in which the government forms a policy by itself and asks the citizens to follow it. However, creating a dialogue mechanism will make things move much quicker and faster," he says. Singh views that this will help raise the level of enthusiasm of the private investors in DFS and also assist in resolving the market related issues quickly.

It is also important to develop the market structure of the Nepali financial sector to effectively deliver the digital services that are aimed at broadening the financial inclusion.

Rather than providing subsidy or opening few branches, it is better to focus on providing technical assistance to the financial institutions to start DFS. "There are many private sector investors in Nepal willing to invest in DFS. We are ready to provide technical support and to help them to learn from other countries and companies. We also look to assist them to start small pilot projects so that they can become more independent," he says.