After a major structural change some three years ago, Neco Insurance is treading a strategic path to achieve unprecedented success in the non-life insurance industry.

--BY NIKEETA GAUTAM AND MAMATA THAPA

Ashok Kumar Khadka

Ashok Kumar Khadka

Deputy CEO

Neco Insurance

Established in 1994, Neco Insurance expects to become the most preferred general insurance company in Nepal. The company which is promoted by Rastriya Banijya Bank, Mahato Group, Vinayak Group and Fund Management Company Limited has not only undergone a major structural change in its capital structure and management, but has forged a network partnership for Nepal with the American Insurance Group (AIG) and boasts a strong financial position in the market with a vision for superior business performance in the future.

Financial Highlights

Four years ago, Neco Insurance’s major challenge was its low capital base. “There were concerns about the level of paid-up capital since the beginning. We were committed to raising the paid-up capital to Rs one billion, whereas only Rs 250 million was the minimum paid-up capital requirement as directed by the Insurance Board (IB),” says Ashok Kumar Khadka, Deputy CEO of Neco Insurance. He believes that the capital structure of insurers should be strong enough to send a positive message to the market. “A strong capital base also increases risk bearing capacity,” he stresses.

In the last three fiscal years, Neco has distributed 45 percent bonus shares and 250 percent right shares to its shareholders. In FY2016/17, Neco issued 10 percent bonus shares and 50 percent right shares to increase the paid-up capital to Rs 1.17 billion. “Though non-life insurance companies are mandated to increase their paid-up capital to Rs one billion by mid-July 2018, Neco’s capital figure will reach the 1.17 billion mark before the deadline,” shares Khadka.

Similarly, Neco’s premium collection reached Rs 1.35 billion in FY2016/17 from Rs 442 million in FY2013/14, a growth of more than 200 percent over the period of three years. The company’s target in the current fiscal year is to achieve earnings of Rs 1.80 billion.

The company in the second quarter of the current fiscal year logged a net profit of Rs 116.5 million and a gross premium collection amounting to Rs 809 million. “Our financial performance in the second quarter clearly shows that Neco is the second largest profit generator among the private sector general insurance companies,” Khadka claims.

A tough stage

Neco Insurance has faced many ups and downs in its journey. For many years, the company struggled to move ahead while competitors started outperforming it. Much of the company’s lackluster performance is attributed to the incompetence of its previous promoters. The company faced a significant challenge in raising the minimum paid-up capital requirement to Rs 250 million as per the directive issued by the Insurance Board (IB) in 2011. The promoters denied injecting more capital in the company which limited its risk taking abilities and the growth prospect for the years to come.

According to Khadka, the company’s momentum was sluggish for many years due to the myopic vision of promoters, internal conflict among them and lack of aggression in business. Rastriya Banijya Bank (RBB), Machhapuchhre Bank, Agriculture Development Bank and Nepal Share Market were the initial promoters of Neco Insurance. “Since banks were our major investors, most of the businesses were derived through them. Due to this, thepromoters and management were passive about exploring new avenues of business and expanding the market presence of the company,” says Khadka.

In recent years, the shareholding structure of the company has changed drastically. Mahato Group now is the major stakeholder in Neco Insurance with 20.24 percent followed by Rastriya Banijya Bank at 20 percent, Binayak Group (12.94 percent) and Fund Management Company Limited (4.51) percent. The changes in the board of directors and management have taken the insurer to a new direction of growth and profitability. The company has been gradually adding infrastructures to strengthen its presence in the market.

Now, Neco has acquired its own land where the company is constructing its corporate building.

Speedy Claim Settlement

Neco has been reliable insurer since its inception. The company has a strong track record in providing hassle free services and speedy claim settlement due to which it has earned many loyal customers. “We have clients who are associated with Neco for the last 20 years,” mentions Khadka.

Adding to its strength, the company introduced the ‘On-the-Spot’ payment policy two years ago. Under this, Neco representatives immediately visit the damage site of the insured property to assess the situation and check the authenticity of the quotation/claim and offer a figure for on- the-spot settlement. If clients aren’t satisfied with settlement offers, they can ask for surveyors. “The documents for claims presented by our policy buyers will be cross checked by the surveyor and will be settled accordingly,” shares Khadka.

Till the second quarter of the current fiscal year, Neco had a claim settlement rate of 47 percent of its total outstanding. “Other companies had a claim settlement rate of 30-35 percent,” says Khadka. According to him, the lower rate of settlement or higher outstanding claims indicate passiveness of other companies in claim settlements. “Our outstanding claims is around Rs 320 million while there are companies with staggering outstanding figures of around Rs 800-900 million to more than Rs one billion,” reveals Khadka.

In the last two quarters of the current fiscal year, out of the total claims settled, the company has settled claims via the “On-the-Spot” basis amounting to Rs 80-100million- around 32 percent of the claims made. Khadka is confident that 95 percent of the customers who received such settlements are satisfied.

Speedy settlement of claims is among the key business strategies of Neco Insurance. “Understanding the market dynamics is vital if we want the market to work in our favour,” opines Khadka. A mentality still prevails in Nepal that insurance companies don’t settle claims timely and the whole settlement process is too time-consuming and tedious. “We take a flexible approach in our claim settlement procedures to ensure satisfaction of the customers. Such approaches have helped us to clear up customers’ views on insurance companies by delivering swift and simplified claim settlements,” Khadka explains.

Khadka says that the strategy of speedy claims settlement is also in line with the company’s aim of maintaining a sound financial position. “Whenever claims are made, 115 percent of the claims have to be provisioned in the books. Timely settlement of a claim means that 15 percent profit can be booked in the accounts immediately,” Khadka says. According to Khadka, making calculative investments on its equity and premiums is another strategy that Neco has adopted to achieve sound financial health.

Other Strategies

Neco has adopted the ‘blue ocean strategy’ of creating a new market space. “The current scenario is such that there are 20 general insurance companies vying for the same market size. General insurers have not been able to cover more than 5-7 percent of the overall non-life insurance market. We need to identify sectors and areas with less or no insurance coverage,” shares Khadka. In line with creating new market space, Neco plans to extend its presence in remote areas such as Panchthar, Phidim, Dailekh, Dadeldhura and Darchula and other similar regions where there is no insurance penetration.

International Partnerships

The company has started collaborations with large insurance multinational companies to solidify its market presence and introduce internationally practiced insurance procedures and products. One of Neco’s recent achievements is its partnership with AIG, one of the top five insurance companies in the world that works with around 80 percent of the Fortune 500 companies. “This landmark partnership will now enable us to establish insurance relationships with MNCs operating in Nepal and any Fortune 500 company entering Nepal. On behalf of AIG, Neco has already taken approval from the Insurance Board for insurance policies that have never been practiced in Nepal including Director and Officers Liability Insurance (D&O) and Public Liability Insurance Policy,” informs Khadka.

Neco has partnered with various foreign reinsurance companies. Its partners in reinsurance include Sirius International UK, ZEP RE and Kenya Reinsurance Corporation, East Africa Reinsurance Company Limited, General Insurance Corporation of India, The New India Assurance Company Limited, Asian Reinsurance Corporation,The Oriental Insurance Company Limited, Societe Tunisienne D, Assurances and Gic-Bhutan Re Limited. Meanwhile, it has also joined hands with the domestic reinsurer Nepal Reinsurance Company Limited.

Growing Market Penetration

Neco is the second largest general insurer in terms of market penetration with 132,000 policies issued by the end of the second quarter of the current fiscal year. “Although Neco stands fourth in terms of premium collection, we have more policies than the companies who stand in second and third positions. It clearly shows the growing market penetration of our company,” says Khadka.

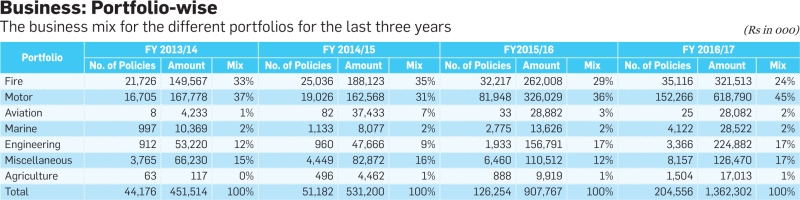

Khadka attributes the company’s success in issuing such large numbers of policies to its focus on retail insurance which he considers as Neco’s other key strength. “Most of our premium comes from retail policies that generate small amounts of premium,” Khadka shares. Neco’s portfolios include motor, fire, engineering, aviation, marine, agriculture and other miscellaneous sectors. “Our major risk coverage is in motor insurance followed by fire and engineering insurance. Our gross premium portfolio for FY2016/17includes 45 percent of our premium coming from motor insurance followed by 24 percent from fire and 17 percent from engineering,” shares Khadka.

At present, the company provides its services through 63 outlets that includes branches, units and contact offices across the country. In the last few years, Neco has increased its presence aggressively with its outlets reaching from 13 to 63. In the current fiscal year, Neco planned to open only three outlets, but has already surpassed its goal by establishing nine branches.

Similarly, the company has introduced Mobile Insurance which enables the policy buyers to pay their premiums through their mobile phones. It has inked agreements with Nepal Investment Bank Limited and Machhapuchhre Bank with a view to sell its insurance products using the mobile app of the commercial banks. “We are also in talks with two other banks,” states Khadka. Meanwhile, Neco has signed ‘bancassurance’ agreements with different commercial and development banks including Machhapuchchhre Bank, Janata Bank, NIC Asia bank and Muktinath Bikash Bank.

Human Resource

At present, there is a lack of human resource in the insurance sector which has been constantly growing over the last few years. “On one hand, there is high staff turnover. On the other hand, there is ashort supply of human resource. The production of the required human resource for the insurance sector is less compared to the growing number of insurance companies in Nepal,” says Khadka.

Neco has adopted different strategies in human resource management to mitigate the associated challenges. “The experienced human resource that we hire is 10 percent of our total staff requirement. Rest of the staff is fresher. They are provided with immediate training according to our business needs and further growth opportunities,” states Khadka. “From the investment perspective, it is a costly way of managing human resource as we don’t know who will stay or not in the future. There is no alternative but to focus on training the untrained,” he adds. Khadka is of the opinion that lack of specialised and practical academic courses and training institutions in the field of insurance has exacerbated the problems for insurance companies.

CSR activities

Neco Insurance is engaged in various CSR activities. The company is a regular organiser of an annual futsal event for bankers and donates the proceedings as charities. “Such programmes help the company to achieve visibility and recognition at the social level on a regular basis,” says Khadka. The company recently provided free one year insurance coverage to an orphanage and has been contributing to the welfare of differently abled individuals. According to Khadka, it is quite difficult for Neco to go for massive CSR activities like commercial banks, but is engaged in executing its part of social responsibilities according to the company’s potential.

SWOT Analysis

Strength

- Capital base

- Focus on retail business

- Strong promoters

- Dedicated staff

Weakness/Areas Need to Improve

- Business with few corporate sectors

- Scarce human resource

Opportunity

- Low level of non-life insurance market coverage

Threat

- Unhealthy competition among the insurers