The worsening spiral in scarce liquidity is rearing its ugly head again. And financial experts blame past government mistakes with no efficient solution in sight.

--BY SANJEEV SHARMA AND SABIN JUNG PANDE

Times are hard for Nepali banks and financial institutions (BFIs). They have been struggling with the ongoing shortage of loanable funds which started in December 2017. From construction of hydropower projects, industrial expansion, real estate and housing transactions to sales of vehicles, many commercial, infrastructure development and manufacturing activities have been hit by the problem.

Mounting Challenges in Liquidity Management

Such problems have become frequent since 2010 when BFIs for the first time found themselves between a rock and hard place due to the acute shortage of cash. The years following 2010 have witnessed such recurrences in high and low magnitudes with a deepening of the crisis particularly in the last two fiscal years. The reason behind this is the high demand of credit and insufficient supply of money which is largely dependent on growth of deposits. In its recently published Nepal Development Update, The World Bank has stated that the growth of money supply in Nepal at present is at a record low level. “Money supply growth has slowed because of no contribution from net foreign assets and a slowdown in private sector credit growth. At 13.5 percent (y-o-y) in February 2018, money supply growth is the lowest in recent years,” says the bank.

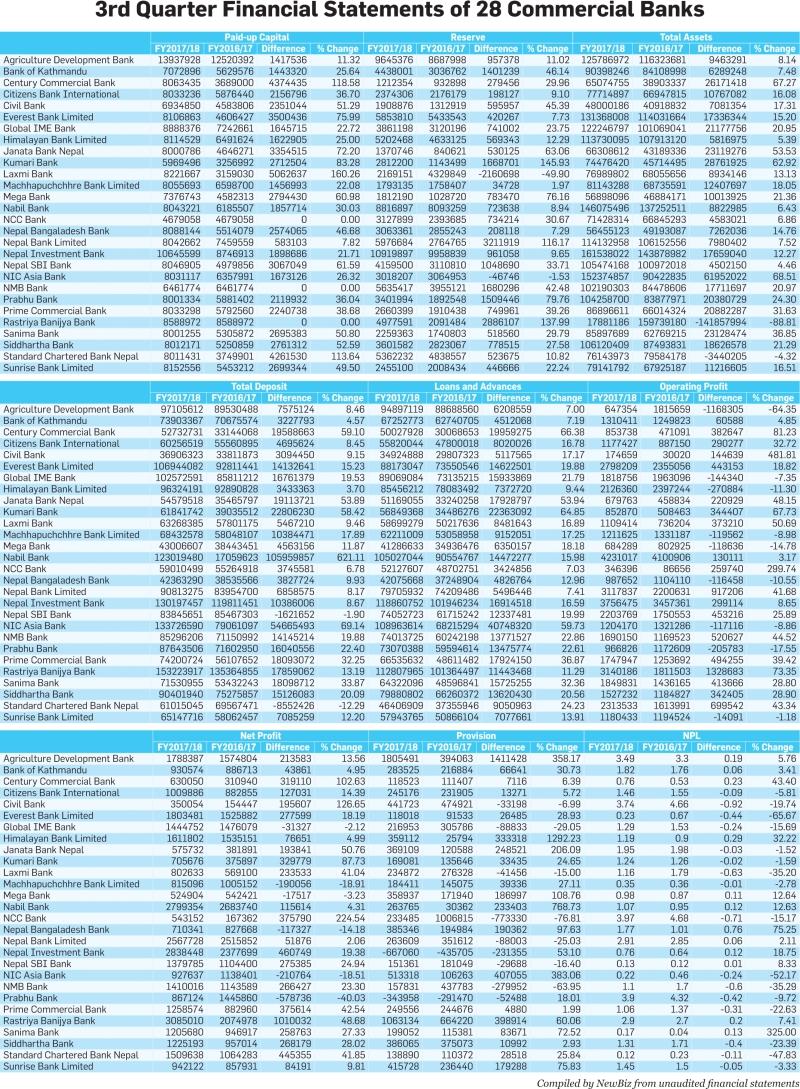

After the end of the Indian embargo in early 2016, industrial and commercial activities resumed and the post-quake reconstruction gained momentum. This led to a situation where businesses in the country needed additional capital to overcome the losses that they faced due to the dual shocks of the earthquake and months long Terai stir in 2015. Pressurised also by the new paid-up capital requirements set by the central bank and growing demand of credit for business and personal purposes, the banks went on aggressively to disburse loans hoping for high profits. The unaudited financial statements for the 3rd quarter of the current fiscal year published by 27 commercial banks show that their loan disbursements have totaled Rs 1.99 trillion compared to Rs 1.64 trillion in the corresponding period of FY2016/17. Meanwhile, deposit collection has amounted to Rs 2.26 trillion in the 3rd quarter of the current fiscal year against Rs 1.85 trillion in the same period of the last fiscal year.

Causes and Ramifications

In a round table discussion organised by New Business Age in late March,high ranking officials of the government, central bank, bankers, representatives from the business community and experts came together to talk about the causes, ramifications of the problems in liquidity management and ways to address the prevailing issues. The participants agreed that the current problems related to liquidity management in the Nepali banking system is basically a result of a heterogeneous mix of factors from sluggish capital expenditure, high government borrowing, mandatory paid-up capital increment of BFIs, high capital demand in the country after 2015, declining remittance growth, a ballooning trade deficit and massive credit demand as well as cash held in the informal economy and increased liquidity preference of the people and businesses.

Speaking on the occasion, Gyanendra Prasad Dhungana, president of Nepal Bankers’ Association (NBA), the umbrella organisation of Nepali bankers, asked the stakeholders to become clear about the nature of the current problems in the banking system so as to avoid confusion and focus on the required areas while addressing the issues. “Many say it is not a problem of liquidity. But banks say they don’t have enough money to lend. No country in the world faces a shortage of loanable funds under normal circumstances. I think, we are yet to face the problem of liquidity. So, it is a unique situation,” he said.

Sluggish Capital Expenditure

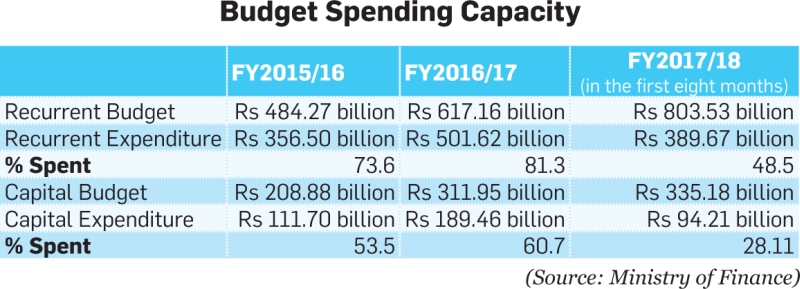

Regardless of their evergreen commitments, successive governments in Nepal have failed to expedite the capital expenditure hence affecting the development works and slowing the money flow into the banking system. The government, in the last eight months of the current fiscal year, has made a capital expenditure of Rs 94.21 billion which is 28.11 percent of Rs 335.18 billion allocated in the development budget. The budget earmarked for development works for the current fiscal year will be actually spent if Rs 1.8 billion is spent on a daily basis during the remaining four months. It is estimated that the actual capital expenditure will be somewhere at 70-75 percent by the end of FY2017/18 which was 61 percent in the last fiscal year.

The surge in government borrowing in recent years also shows the government’s inefficiency in fund mobilisation which has added to the woes of the country’s financial system. According to the World Bank, government borrowing reached Rs 365 billion in 2018, even as its deposits balance in the NRB account stood at Rs 302 billion. “The government borrowed from the market primarily to fund the fiscal transfers of the local bodies. However, as the spending of the local bodies has been low so far, the government deposits at the account of local authorities of the central bank have increased. These deposits, which are held at the NRB, effectively remain outside the banking system, and have contributed to creating and sustaining the credit squeeze in the financial system,”reads the Nepal Development Update. The World Bank likened the government borrowing to the ‘mop-up’ operations of NRB which the central bank conducts in a situation of excess liquidity in the market.

Meanwhile, the mobilisation of bank deposits of government institutions is also largely ineffective. “Out of a total deposit of Rs 2,500 – Rs 3,000 billion in the Nepali banking sector, deposits of around Rs 1,400 billion is institutional, mainly coming from government institutions,” mentioned Hari Bhakta Sharma, president of the Confederation of Nepalese Industries (CNI), adding that, unless the government builds an effective mechanism to mobilise such funds, the loanable fund crisis will keep on recurring.

Hyper-dependence on Remittance and Imports

The overdependence on remittance has led Nepal to a place where a decline in remittance can cause problems in the financial system. 2017 saw the steepest decline in remittance growth in 10 years. The remittance inflow totaled Rs 699 billion in FY2016/17 while the growth rate slumped to a mere 5.10 percent from 7.74 percent and 13.62 percent in 2016 and 2015 respectively indicating the saturation of remittance inflow. This is primarily due to a decrease in the number of migrant workers going abroad.

Sharply increasing imports on the back of remittance-fueled consumption are also among the reasons for the shortage of investible funds in banks. According to a report published by NRB, in the first seven months of the current fiscal year, the import of merchandise goods amounted to a staggering Rs 661.2 billion, up 18.9 percent from the corresponding period of the last fiscal year. Exports, meanwhile, were flat during the review period totaling just Rs 47.6 billion.

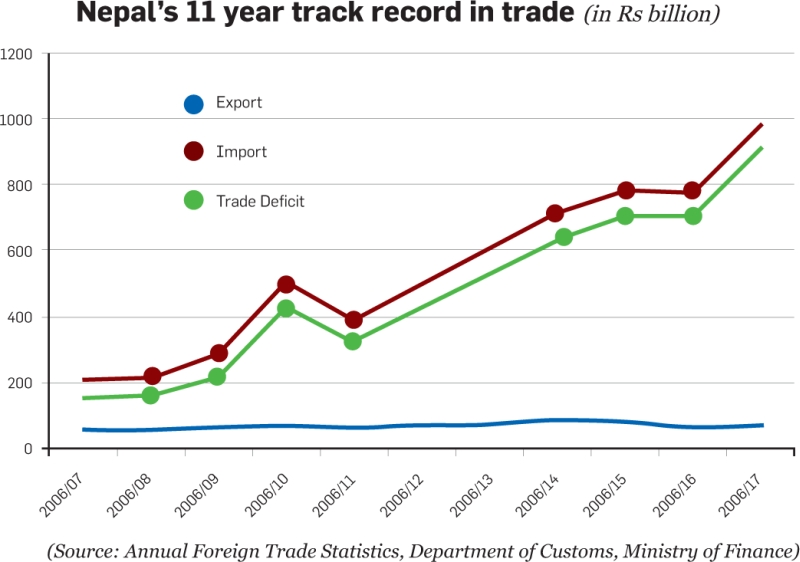

Over the last 11 fiscal years, Nepal’s import value has risen drastically by around 362 percent from Rs 213 billion in FY2006/07 to Rs 984 billion in FY2016/17. The trade deficit has widened dramatically in the years following 2006, increasing almost 500 percent from Rs 154 billion in FY2006/07 to Rs 911 billion in FY2016/17. In all these years, export figures haven’t, even once, crossed the figure of Rs 90 billion.

This indicates that the money Nepal receives as remittance is spent in imports and does not stay in the country’s banking system. Businessman Rajendra Kabra sees the recurrence of problems in liquidity management as a result of successive governments’ priorities in state revenue growth neglecting the country’s GDP growth. “It is an irony that the government’s revenue growth target is over 30 percent in a country like Nepal where the GDP growth is less than seven percent,” he said.

The Black Money

Many believe that funds mobilized during last year’s election campaigns are yet return to the financial system. It is feared, lot of that money will not return to the formal system because it was spent and earned illegally. However, Nepal Rastra Bank’s Deputy Governor Chinta Mani Siwakoti says, “We are yet to see how long such money will be parked in the personal vaults.” Hinting about the recent call to provide an opportunity to some members of the business community to make a self-declaration of wealth, Siwakoti indirectly responded by asserting that NRB will never concede to such demands. “They should think what will happen to such funds if we execute demonitisation as India did. Although we haven’t thought in that line, it can’t be ruled out as a future intervention,” said Siwakoti.

Nevertheless, stringent anti-money laundering (AML) rules are also behind the low deposit collection of banks. While stricter AML compliance has become quite necessary for Nepal in the present day context to increase its credibility internationally, not many Nepalis have the documents to clearly show the source of their income due to the legal system of the past, say stakeholders. According to them, many in the past have earned large sums of money from legitimate sources, but weren’t properly documented or even were undocumented at all as the law in those days did not require that.“People have stopped depositing their money in BFIs due to the anti-money laundering (AML) arrangements that require depositors to verify the source of amounts of over Rs one million,” said Kamalesh Kumar Agrawal, vice president of Nepal Chamber of Commerce. He opined that many people don’t have documents to verify that their money isn’t generated from illicit sources. “This is another reason for sluggish deposit growth of banks in recent times,” he said.

Behind the Risk Taking Appetite of Banks

Despite their role in changing the economic face of Nepal and increasing access to modern banking services among Nepalis, banks have not remained saints regarding the present day problems. The focus of banks on earning profits has led them to take risky maneuvers in terms of loan portfolio expansion and investing a big chunk of their capital into the so-called ‘unproductive sectors’ such as auto, real estate and stock market. This has caused some serious issues in terms of compliance of prudential regulation of banks.

After the NRB set the new minimum paid-up capital for BFIs in 2015, the financial institutions aggressively engaged in lending which has several times outpaced their allowed limit. The credit expansion drive has led BFIs to near the limit set under the credit-to-core-capital-and-deposit-ratio (CCD). In the third week of February,CCD ratio of some commercial banks jumped to 79 percent. The mandatory provision of the central bank restricts banks to extend loans beyond 80 per cent of their CCD levels.

Moti Lal Dugar, chairman of MV Dugar Group and Sunrise Bank links the lending spree of banks to the cost of capital. “When there was availability of funds, banks were lending at the rate of 6-7 percent. When the cost of capital in the developing countries like ours is low, people tend to take higher risks and invest recklessly,” he said, adding,“It is high time the central bank place a cap on unproductive investments and clearly differentiate what is productive and what is not.”

It is often argued that it is natural for banks to have an increased appetite for lending once their capital has increased. It is what banks are there for. Profit-making institutions such as banks wouldn’t want to lock up their money at vaults just because the real sector of the economy has lower demand for capital.

Yet, it cannot be fully discarded that the current crisis has its roots in the way banks have been performing. Kewal Prasad Bhandari, joint secretary at Ministry of Finance insists that a large portion of bank lending is made in unproductive sectors which has made liquidity crisis a frequent episode.

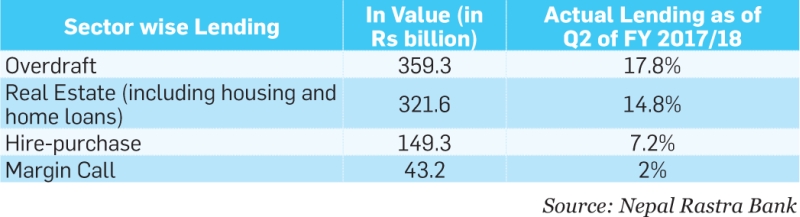

According to the Nepal Rastra Bank (NRB), BFIs have an outstanding lending of Rs 918.4 billion in overdraft, real estate, hire purchase and margin-type loans as of the second quarter of FY2017/18, accounting to 41.6 percent of their total outstanding loans.

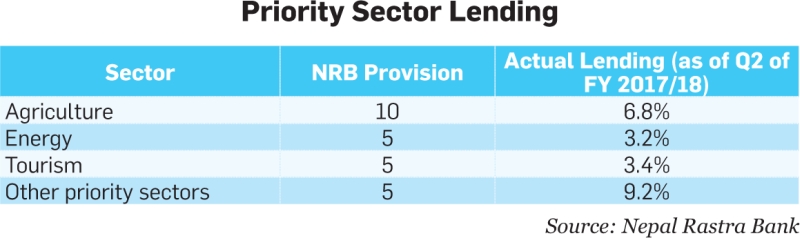

In a bid to curb such practices, the central bank has already directed banks to contain their over exposure in unproductive sectors. Recently, NRB introduced a new provision mandating the banks to cut back their overdraft financing to 15 percent of their total lending. Also, commercial banks are required to allocate a minimum 25 percent of total credit to the priority sector, including at least 10 percent to agriculture and five percent each to hydropower and tourism and the remaining five percent to other priority sectors. According to Chinta Mani Siwakoti, Deputy Governor at NRB, “A number of banks have failed to comply with NRB’s provision of 10 percent lending in agriculture with some failing to even cross the mark of five percent. We feel that such banks need to be reprimanded.” Siwakoti is of the view that the allocation for the energy sector should be increased to 10 percent of the total lending from the existing five percent.

Risk to Banking Good Governance

The minimum paid-up capital increment drive coupled with high capital demand, low deposit growth and shortage of investible funds has been affecting the good governance practices in the banking sector. As the bank promoters have been adding additional money to meet the statutory paid-up capital requirements, CEOs are feeling the heat to maximise profits by any means. Banking industry insiders claim that promoters are unnecessarily interfering in the day-to-day operations of banks at present. The departure of some bank CEOs in recent months is said to be the result of the rising conflict between the board of directors and upper management.

However, Sunrise Bank chairman Dugar refutes these interference claims. “It is completely false that the boards of the banks are pressurising their managements for high profits to match the increased paid-up capital,” he expressed. According to Dugar, promoters have been strictly following NRB’s directives that completely bar board interference in the management.

Other problems in the banking sector have also come to the fore in the wake of the deepening short supply of lonable funds. The bitter interest rate dispute between the banks over the last few months is one such example. It started after the Nepal Bankers’ Association and one of its members, NIC Asia Bank, entered into a row over the new interest rate on fixed deposits and savings accounts set by the latter in the second week of March. The issue was resolved after a few days. The association in early January capped the interest rates on fixed deposits at 11 percent and savings at 8 percent which has continued till date. The move was aimed at curbing the competition among banks in deposit collection and bringing ‘interest rate stability’ in the market. Nonetheless, the association has faced backlash from various quarters against its step which, according to the opponents, is an ‘anti-competitive act’ going opposite to the norms of the free-market economy.

Rajan Singh Bhandari,CEO of Citizens Bank International agrees that the interest rate dispute has created problems in the banking sector.“The central bank should play a vital role in this regard. Time has come for the regulator to adopt a mechanism to indicate desired interest rates,” said Bhandari.

Business Sector Problems

The Nepali business fraternity has been struggling with the mounting challenges. “On the one hand, financing in the productive sector has been declining. On the other hand, operational costs of industries are increasing,” said CNI President Sharma. “Industries can’t pass the increased costs to their end consumers right away. If they do so, their competitive edge will decrease,” he added. According to him, in such a scenario, it doesn’t seem wise to make investments in Nepal when the production costs are high and bank financing is either unavailable or unviable.

At present, hydropower is among the sectors badly affected by the current problems. Hydropower entrepreneur Guru Prasad Neupane puts it like this, “We, the hydropower entrepreneurs are stuck in a hole. The rate fixed in the Power Purchase Agreement (PPA) does not increase. And it is an irony that the notice of banks regarding the increment in interest rates on loans comes three to four times a year.” According to him, it has been quite hard for hydropower developers and investors to pay interest rates on loans which now are hovering over 14 percent.

The way Ahead

Mobilisation of foreign capital is increasingly becoming a viable short-term option for commercial banks in Nepal to ease the difficulties in their liquidity management. Last month saw three commercial banks, namely NIC Asia, NMB and, Himalayan Bank and Global IME sign loan agreements with the International Finance Corporation (IFC). “Nepal banking system needs Rs 200-300 billion additional money immediately. There is no alternative for us other than to borrow money from foreign banks to ease the problems in liquidity,” said Sunil KC, CEO of NMB Bank. He informed that another 4-5 international banks are also in the pipeline for such borrowing.“NMB Bank has adopted the principle of “value based banking”. Under this, our focus is on increasing investments in productive sectors,” mentioned KC. He suggested the central bank come up with a hedge fund arrangement for borrowing foreign money to mitigate the risks posed by fluctuations in foreign exchange rates.

Another short-term solution can be the abolishment of CCD ratio as suggested by Nepal Bankers’ Association President Gyanendra Prasad Dhungana. “The banking system can have an additional Rs 154 billion as loanable funds if the CCD ratio is removed and only CRR and SRL are used for control. However, such a move can only provide temporary relief,” he said, adding, “Therefore the focus of all stakeholders should be on bringing foreign capital to address the current problems in the country’s banking sector.”According to Santosh Koirala, Acting Deputy CEO of Machhapuchhre Bank Limited, fresh capital can come into the financial market if there is an arrangement for government offices to open their accounts in the commercial banks. “They are allowed now to have accounts only in the central bank. This is likely to ease the problems in liquidity to some extent,” he opined.

Meanwhile, attracting FDI carries the prospects of a long-term solution to the current problems. Nonetheless, the FDI realisation in fact is miniscule compared to the investment commitments worth billions of Dollars made by foreign investors over the years. For example, in the first seven months of the current fiscal year, FDI inflow amounted to Rs 14.3 billion, up 89 percent from the corresponding period of last fiscal year. However, the inflow is less than one percent of country’s GDP.

The situation is likely to recede after the government speeds up capital expenditure as the current fiscal year is nearing the end. But the scenario has become such that it is quite hard to predict that there won’t be a scarcity of investible funds next year. Facing difficulties in liquidity management is not a new problem for the country’s banking sector. Now the time has come for the government, central bank and BFIs to learn from past mistakes and take decisive steps in order to ensure this problem, which can jeopardize the overall economy, won’t reoccur.