Leveraging existing network of BFIs, NCHL is facilitating the development of national payment systems

Neelesh Man Singh Pradhan

Neelesh Man Singh Pradhan

Chief Executive Officer

Introduction

Promoted by Nepal Rastra Bank (NRB), commercial banks, development banks, finance companies and Smart Choice Technologies Pvt Ltd (SCT), Nepal Clearing House Ltd (NCHL) was establishedon 23rd December 2008 to implementmultiple national payment, clearing and settlement systems in the country with an aim to establish national payments gateway.Itselectronic cheque clearing system (NCHL-ECC) is in operation through 109 member banks and financial institutions (BFIs)with over 2,775 branches network. And it recently launchedthe Interbank Payment system (NCHL-IPS)that provides safe and efficient means of funds transfer from one account o any other account held at any of the participating 63 member BFIs with over 2,000 branches.

NCHL launched its NCHL-ECC system in February 2012 and the nationwide rollout was completed in next one and half year. According to Mr. Neelesh Man Singh Pradhan, CEO of NCHL, the company rolled out the NCHL-ECC system successfully by replacing the old manual process of cheque clearing being facilitated by Nepal Rastra Bank to the BFIs. As the second larger payment infrastructure, NCHL launched NCHL-IPS system since August 2016 that supports both direct credit (payments) and direct debit (collection) related transactions.

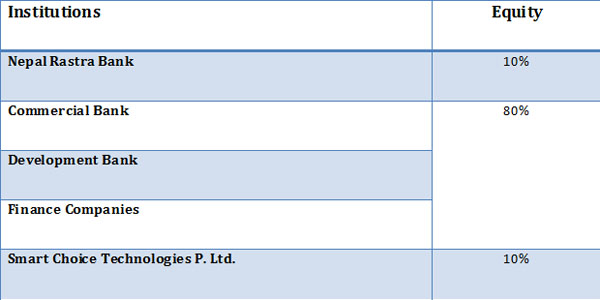

NCHL Ownership

NCHL has ensured that along with its operations, the ownership structure of the company is also equitable to the major stakeholders. It is owned by the Nepal Rastra Bank, Commercial Banks, Development Banks, Finance Companies and Smart Choice Technologies P. Ltd.

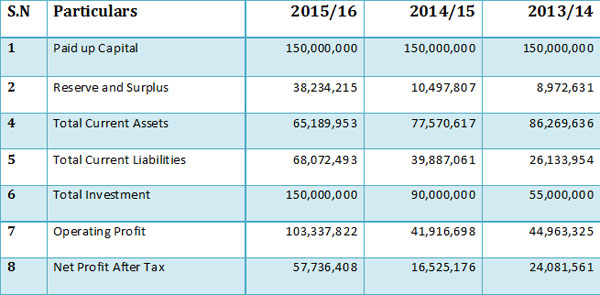

NCHL Financials

Growth Trend

Started with just two staff members, the company is now successfully running its operations with 15 strong member staff supporting over 4,700 users of the participating member BFIs. The cheque transaction in NCHL-ECC system has also increased from less than 10,000 cheques per day initially to over 36,000 cheques per day, which translates to over NRs 15.5 billion in average daily settlement value. The transactions volume and value in NCHL-IPS is also started picking up within few months of its operations

According to Mr.Pradhan, NCHL’sbusiness has been growing well both operationally and financially. “Initially, it was projectedthat the company will take around four and a half years to reach the break-even.But the companyachieved the break-even within the third year itself and starting making profit,” he says. The increase in the transaction volume, well reflecting the acceptability of electronic cheque clearing and the number of member BFIs in the NCHL-ECC has led to the growth of company’s business.“The operating profit of the company grew by 146% and the net profit grew by 249% in the fiscal year 2015/16 compared to the previous year," mentionsMr.Pradhan.

Products and Services

NCHL has established a core payment infrastructure through which it services its members. Currently the available payment systems include NCHL-ECC system and NCHL-IPS system.

• NCHL-ECC: It is an image-based, cost-effective, MICR (Magnetic Ink Character Recognition) cheque processing and settlement solution where an original paper cheque is converted into an image for electronic processing of the financial transactions between participating member BFIs. The physical movement of the cheques are truncated or stopped at the level of the presenting bank in the NCHL-ECC System. The cheque does not physically travel to the clearing house or to the paying branch as it used to do in manual clearing process, resulting in a faster and easier processing of the cheque transactions.Regular, High Value and Express cheque clearing are currently available through this system with same day settlement.

• NCHL-IPS: It is a system to safely and efficiently transfer funds from one account to any other account held at any of the participating member BFIs. It supports account to account payments (Direct Credit) and collection (Direct Debit) related transactions. The underlying transaction could be for various purposes defined as products and currently supports customer transfer, treasury transfer, government payments, remittance, dividends, IPO refund, salary payment insurance premium payment, instalment payment and credit card payment.Mandate based debit instructions can also be processed through NCHL-IPS system

"These systems provided by NCHL have made payment processes convenient, faster and cost saving for the customers,” mentions Mr.Pradhan.

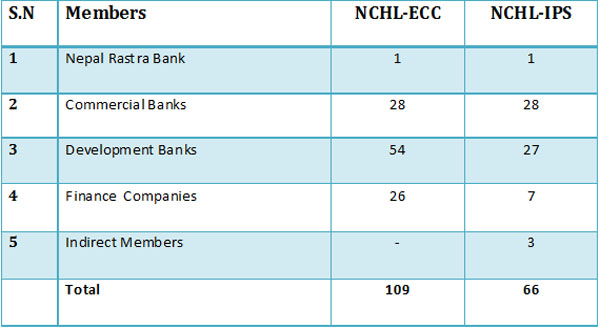

NCHL Members

NCHL-ECC and NCHL-IPS systems are governed by the Operating Rules issued by Nepal Rastra Bank, which also defined the process for participating in the systems operated by NCHL. NCHL currently has only BFIs and NRB as its members of NCHL-ECC system, who are allowed to issue cheques. Whereas, in the case of NCHL-IPS system, BFIs are enrolled as Direct Member and other non-banking financial institutions and other large institutions are enrolled as Indirect or Technical Member. Indirect/ Technical members can directly initiate their payment transactions with little dependency with their banks thereby increasing efficiency and convenience.

Total membership base of NCHL is as follows:

SWOT Analysis

Strength

• Promoted by NRB and BFIs

• Large membership base withwide bank/ branch network

• Technical infrastructure with strong team

Weakness (Scope of Improvement)

• Enhance and upgrade existing infrastructure and technology.

Opportunities

• Payment industry in Nepal being at an initial stage provides lots of opportunities.

• Increasing acceptability of electronic payments by the market including end customers, business and government.

Threats

• Merger and acquisition of BFIs will reduce membership base.

• Possibility of increasing competition due to recent change in payment system policy.

• Continuous changes in technology

Future Plans

In line with NCHL's product/ service roadmap that it has set for itself, it will implement and operate multiple national payment systems in the country. “NCHL will continue to facilitate the development of secure and trusted payment methods and technologies in Nepal.After NCHL-ECCand NCHL-IPS, we have initiated feasibility study of some of the other payment systems and related projects including mobilefinancial services, payment switch and certifying authority," says Pradhan. NCHL intends to develop payment infrastructures by means of reinvestment of its profit generated from the existing systems thereby developing multiple sustainable payment infrastructures.

Corrigendum: The earlier content is changed as per the request of the NCHL as there were some mistakes in the article posted earlier. The mistakes are greatly regretted. We have not done the editing of this content. - Editor